by Tom Walker Deputy Global Head of Listed Real Estate

Last year Investors shifted their preference away from American stocks towards those in Europe; where they saw better value than those across the Atlantic. This theme looks set to continue this year as investors look for value.

At the same time institutional investors stated that they wanted to increase their allocations to direct property. In the last AMP Capital Institutional Investor Report, property was nominated as their favoured asset class.

Given these trends, it is natural that investors are starting to look at the prospects for listed real estate in Europe.

Europe’s economies recovering

Since the global financial crisis (GFC) both the United Kingdom and European economies have been characterised by significant economic weakness. The UK, aided by the ability to make important decisions independently, moved quickly towards austerity policies. The benefit of this relatively quick decision making looks to be paying dividends. The economy is now accelerating back toward a growth trajectory which presents opportunities to position your portfolio for an exposure to growth.

In comparison, continental Europe remains weak, largely as a result of a convoluted decision making process within the Euro area. However, we believe that there are a number of compelling investment opportunities incorrectly priced by the capital markets.

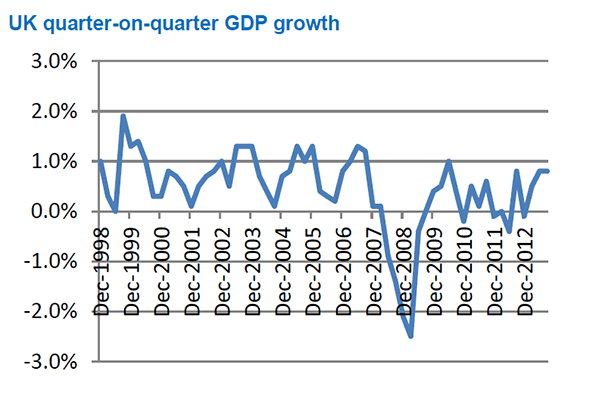

Post-GFC, the UK’s leading FTSE index sold off approximately 50%, and has experienced 16 quarters of negative or anaemic, below trend growth. As a result of this economic weakness and financial stress, very little new property stock has been brought to market which has generated an imbalance and latent demand in the market for product.

The supportive policy environment in the UK has stimulated the economy similar to the US. The economy is now showing signs of a recovery with the most recent GDP figures indicating annualised growth of around.1.9%, far higher than the market’s expectations of 1.5%. The International Monetary Fund believes the UK will have the fastest growing economy in the G7 countries.

Source: Bloomberg as at January 2013.

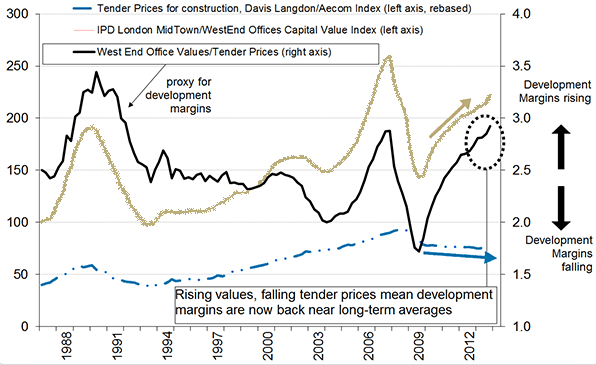

As the UK enjoys a recovery back to growth, property developers are benefitting from margin expansion. Those developers with a capability to commence projects in markets with strong levels of demand are able to provide investors with attractive returns.

Source: Morgan Stanley as at November 2013.

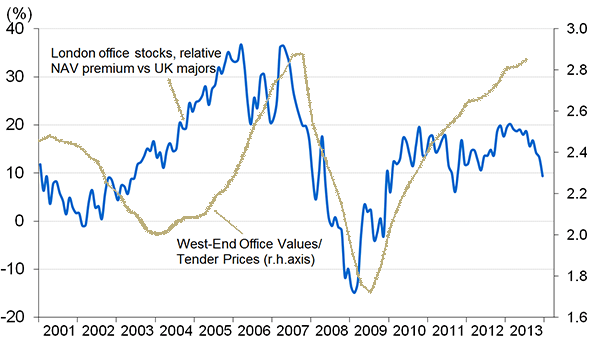

Historic analysis shows that central London property prices can be used as a leading indicator for regional UK assets, and we believe that this property price behaviour will play out as history suggests.

Therefore, as the central London cycle accelerates this economic improvement will ripple out toward more regional areas as a second derivative effect.

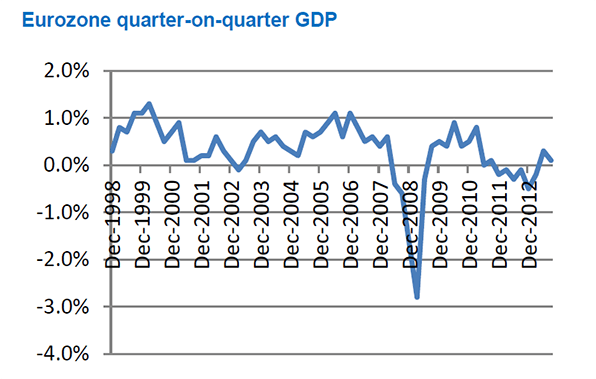

After a significant slowdown in the cycle post-GFC, the property cycle is now at the point where it can accelerate as it has done in the past. In comparison, continental Europe remains structurally challenged, with weak growth and banking issues making for a weary economic environment.

Source: Morgan Stanley as at November 2013.

Despite the significant imbalances within the European area we are encouraged by improving economic indicators. In addition, the European Central Bank has made it clear it will do “whatever it takes” to support the single currency and improve economic growth.

The outlook for European REITs Stocks remain cheap in this environment; the key question however, remains whether they are value traps or real value. Our view is that many of stocks in the EU are value traps and we are therefore tilted towards stocks which hold high quality assets with weak management. These stocks are prime turnaround candidates and we expect to see changes in management teams and strategy over the course of the year. We have identified that there are several such stocks in the real estate sector.

Two interesting examples of our European holdings are Gecina and Klepierre. Both companies have seen a dramatic change in their shareholder register and we believe this has the ability to transform the way these companies are managed to the benefit of shareholders.

Critically both companies have a high quality real estate portfolio that was under managed over the past five years. While the broader European economy is still relatively weak these companies will be able to produce above average returns utilising the skill of new management teams.

Source: Morgan Stanley as at November 2013

Risks We recognise that there are risks to this positive outlook for the European region. Key risks in the UK include an increase in inflation that could shift discretionary income spend away from retail into non-discretionary spend and therefore not flow through to landlords with sales exposure.

There is some evidence of this at the moment, but we don’t believe this is the most likely outcome. The EU faces similar prospects to deflationary Japan. It has a weak economic growth environment of around 0.1% for the quarter, which is not generating enough impulse to drive inflation and inflationary expectations.

Combined with a delicate banking system, the economic conditions in the EU remain challenging. The result of the weak inflationary environment and any further deterioration in the banking system could cause economic growth and spending to curtail further leading to underperformance of the EU against other more attractive regions.

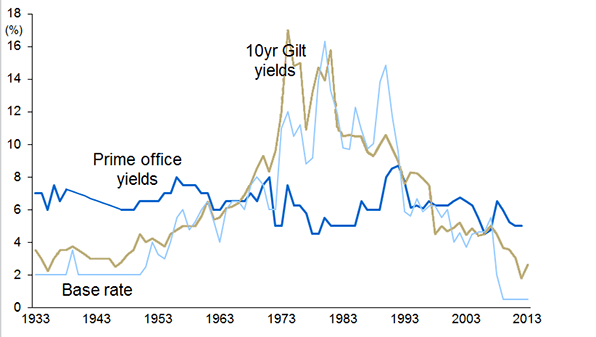

This scenario is not our base case however, given that a supportive policy environment exists. Finally, any outlook is not complete without an analysis of how increasing interest rates might affect the real estate sector. As demonstrated in the graph below, we believe there is little correlation between property values and long term interest rates.

Source: Morgan Stanley as at November 2013.

About the Author

Tom Walker is a deputy global portfolio manager, alongside James Maydew he assists Matt Hoult in all aspects of running the global fund.

He is based in AMP Capital’s London office and is primarily responsible for the coverage of the European listed property sector.