By Tom Walker, Deputy Head of Global Listed Real Estate

23rd January 2014

“The surprise asset class of the next decade could yet be property which became something of a dirty word after 2007. Rental yields are 6% or so in the main markets, an attractive income stream when European corporate bonds yield just 4%. Property yields will benefit if developed markets recover; and it is usually a hedge against inflation,” The Economist 26 January 2013.

There are seven reasons why global listed real estate should be in an investor’s portfolio.

1 – Yield spread over corporate bonds

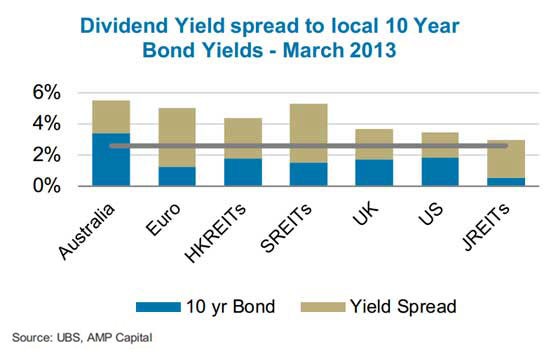

One of the simplest ways to look at the value of real estate is to determine whether an investor is receiving a large enough premium over and above the risk free rate to compensate for the risks involved in real estate investment.

Historically, analysing the spread between the risk free rate and property dividend yields has been a relatively effective way to establish the risk premium in the real estate sector. As shown in the graph below, this simple analysis indicates there is an elevated risk premium in the global sector.

However, it is important to point out that the expansionary monetary policies of central banks around the globe are artificially reducing the risk free rate. Therefore, we believe a more appropriate measure is the spread of property yields to corporate bonds. Currently, the spreads between property yields and corporate bonds, such as BBB+ bonds, has never been wider. 2 – Earnings growth In a low growth environment, it is important to identify those companies that will see their earnings grow in excess of the average real estate participant. In a global portfolio there are multiple real estate markets in which to allocate funds. Despite an uncertain macro-economic environment a number of real estate markets offer investors double digit earnings growth. Higher earnings translate into higher profits and a higher share price. In addition, the tax efficient structure of real estate investment trusts means that higher profits should translate into higher dividends paid, which increases the total shareholder return. 3 – Lower debt costs It is clear that high quality companies are able to access the debt markets at cheaper rates. In October 2012 Nestle issued a bond with a coupon of 0.75% to set the record for the lowest coupon offered on a four year bond in Europe.

In May 2013, the world’s largest listed company, Apple, issued three year debt at a coupon of 0.5% and five year money at 1.0%. Whilst these rates are not lower than the sovereign country in which they are headquartered, the margins are at historic lows. The real estate sector is no different and the sector’s earnings profile continues to be enhanced by lower debt costs. In December 2012, Simon Property Group (SPG) issued $750m of five year debt at 1.5% and $500m of 10 year debt at 2.75%. SPG’s cost of debt was issued at a historically low margin to the US Treasury bonds of the equivalent time period. We are now seeing SPG’s ‘debt experience’ being replicated in many property companies.

Whether they are located in London, Paris, Hong Kong or Sydney it is clear that banks want to lend to high quality companies with strong balance sheets. It is important to point out that whilst a lower cost of debt is beneficial to real estate companies, it is not ‘organic’ earnings growth i.e. created by the expertise of management teams. The strength of a company will dictate whether it can borrow money at a cheaper rate than a competitor. However, we do not see the benefit of lower debt costs as sustainable over the long-term. However, should interest rates rise and the cost of borrowing increase this is likely to occur at a time of increased economic strength and then real estate companies should be able to pass on this increased cost to tenants in the form of increased rents. 4 – Value Whichever real estate market we analyse it is possible to see companies that are both undervalued and overvalued.

The two key ingredients to making the right decision are: 1 – A track record of successful investing 2 – A disciplined investment process. Like successful investors, a number of companies have been able to demonstrate long-term track records of adding value to their portfolio. For instance, Westfield’s experienced management team has successfully traded and developed the right properties at the right time. A company that can consistently create value for its shareholders deserves to trade at a premium to its underlying asset base. 5 – Japan It is impossible to ignore the effects of the Japanese economic policies and the impact they will have on the real estate sector, not only in Japan but globally. The intended result of ‘Abenomics’ (the ‘three arrows’ of monetary easing, fiscal stimulus and private investment growth) is to achieve a 2% inflation target and economic growth. What differentiates the action taken by the Bank of Japan (BoJ) to those taken by other central banks is the scale of the policies, no other central bank has pledged to double the monetary base in two years.

Whatever the outcome of the BoJ’s policies, the outlook for both the Japanese and the global real estate sector is likely to be positive. Success for the BoJ will result in economic growth which leads to businesses growing and an increasing demand from tenants in all sectors of the property market. With increasing demand from occupiers comes rental growth. In addition, if the inflation target is met the index linked income streams will rise along with inflation. This will also lead to increases in the capital values of the assets. Therefore, real estate investors are likely to be hedged from the effects of inflation.

If the BoJ is unsuccessful, the monetary expansion through the acquisition of Japanese Government Bonds (JGBs) is likely to lead to a lower cost of debt for corporates. A lower cost of debt allows for a greater level of earnings to flow through to shareholders. Also in this scenario, low economic growth would make listed real estate a good alternative to JGBs for enhancing the yield within a portfolio without necessarily increasing the level of risk. Other central banks, such as the US Federal Reserve or the Bank of England, are not adopting such aggressive policies.

However, they are still engaged in expansionary monetary policy but over a longer time period. Therefore, it seems logical to expect the same effects which may take place in Japan, over a shorter time scale, will also take place in the US and UK over a longer period. It can be argued that these policies may underpin the pricing of real estate in these markets. 6 – Inflation protection Almost every economic textbook states that when the supply of money increases so does inflation and it appears that the western economies are trying to inflate their way out of high debt levels. The same economic textbooks detail how to hedge investments against inflation with ‘real assets’ such as real estate.

Real estate is one of the few asset classes that offer investors a hedge against inflation for both the income and capital. The income streams derived from the majority of commercial properties are index-linked to inflation on an annual basis. Therefore, the levels of income received and subsequently paid out to shareholders should reflect any increase inflation. The capital value of an asset is also likely to rise in line with inflation. 7 – Consistent yield Over the past 10 years, global real estate securities have delivered a 9.6% annualised total return, outperforming global equities and global bonds1. In addition, a global listed real estate portfolio offers investors a distribution yield of around.4% with forecast earnings growth of more than 6% at present2.

Source: AMP Capital