Dr Shane Oliver Head of Investment Strategy and Chief Economist AMP Capital Investors

Introduction

The problems with the US economy are well known. Its level of public debt is too high, its spending on social security and health is unsustainable, its health system is woefully inefficient – spending more relative to GDP than most OECD countries but with worse life expectancy – its level of savings is too low, its transport infrastructure is becoming run down, its political system seems dominated by ideology and its share market has had a rough time over the last 14 years as the tech and housing credit booms burst.

But it is dangerous to write the US off. Every two or three decades it seems to reinvent itself. It did it with electricity and mass production in the 1920s, with consumerism, petrochemicals and aviation in the 1950s and 1960s and with deregulation and the IT revolution in the 1980s and 1990s.

Don’t write the US off

The US was written off by many during the 1930s only to see it emerge as the world’s major super power and strongest economy in the post war years. The same occurred in the 1970s after the debacles of the Vietnam War, Watergate and stagflation only to see it reinvigorated by Ronald Reagan. Both the 1950s-1960s and the 1980s-1990s saw strong returns from the US share market.

After the debacle of the tech wreck and credit bust of last decade and the loss of its AAA credit rating by S&P, amidst dysfunctional politics, many have been tempted yet again to write the US off. But once more it seems to be bouncing back. This time around the drivers include: American policy makers’ determination to fix their problems; an energy boom; a manufacturing renaissance; and ongoing innovation.

The Fed and the shrinking US budget deficit

American policy makers are criticised a lot, eg for first undertaking quantitative easing and now for slowing it! But they do show a determination to fix things up once they go wrong and for moving a lot faster than other countries. This has been evident since the GFC with the Federal Reserve trying one approach after another to stabilise and then get the US economy moving again and the forced recapitalisation of US banks, which helped restore confidence. That these policies are working is evident in the Fed now moving to slow down its quantitative easing program, effectively taking the US off life support as it appears to be getting to the point where it no longer needs it.

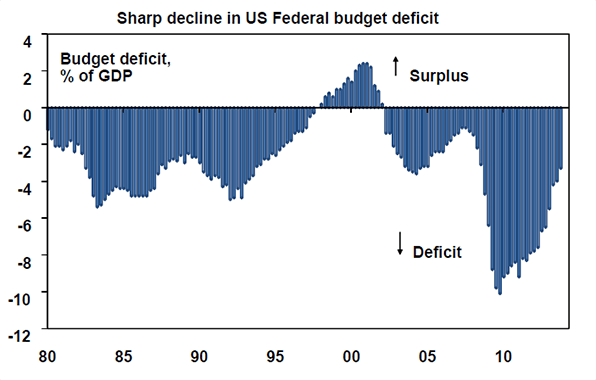

But perhaps the big surprise for many is the massive slump in the US budget deficit over the last few years, which basically explains why you don’t hear much about it these days. As can be seen in the next chart the US Federal budget deficit has shrunk from more than 10% of GDP In 2009 to less than 3% of GDP this year. This reflects a combination of stagnant government spending over the last few years and surging revenue growth.

Source: Bloomberg, AMP Capital

It is expected to start rising again beyond 2015 to around 4% of GDP by 2022 (according to the Congressional Budget Office) as an aging population really starts to boost spending on social security and health, so there is still more to do. But the savings from the 2011 debt agreement, the scaled back “fiscal cliff” and the “sequester” spending cuts add up to almost $US4 trillion over 10 years and should not be ignored. It’s a long way from the fiscal mess of a few years ago.

The energy boom It seems only yesterday that the “peak oil” fanatics were raving on (yet again) about how global oil production would soon peak and we would have to ditch the car and return to the horse and buggy. It was nonsense then and even more so now.

The basic thing they missed is that rising oil prices will both lead to more fuel efficiencies (just look at all the hybrid cars now available) and make economic access to new supplies of energy viable.

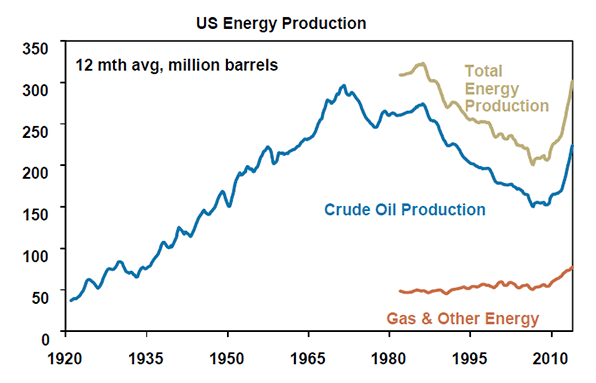

This is happening in the US with a vengeance as fracking technology – drilling down and then sideways into shale beds and then pumping in a mix of water and chemicals to fracture the rock allowing gas and oil to be extracted – is leading to a massive energy production boom.

US oil production is up around 45% over the last five years which has taken it back to 1990s levels and total energy production including gas is back to late 1980s levels. See the next chart. By around 2020, US oil production is likely to have returned to 1970 levels and the US will be back to being the world’s biggest oil producer.

Source: US Energy Information Agency, AMP Capital

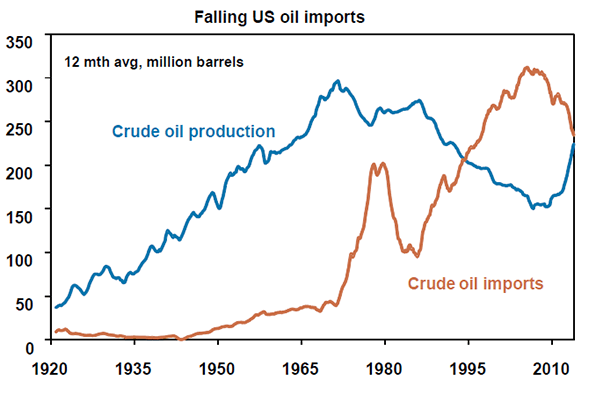

The energy boom is providing a huge boost to the US economy by boosting demand for drilling services and infrastructure, lowering energy costs & reducing the US trade deficit. US oil is trading around $US7 a barrel below global prices and US natural gas prices are tending to run around one third below European levels and one fifth of Japanese levels. Rough estimates put the boost to US economic growth from the energy boom at 0.2% per annum. The decline in US oil imports can be seen in the next chart. This also means less dependence on the volatile Middle East

Source: US Energy Information Agency, AMP Capital

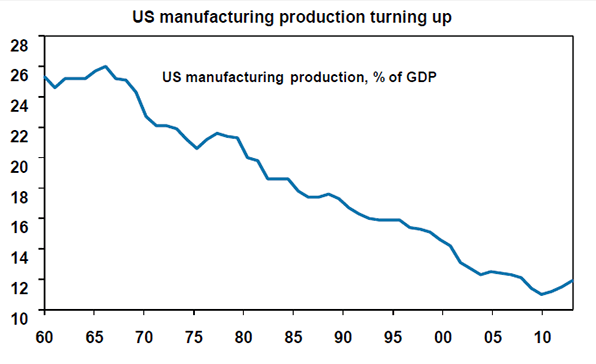

The manufacturing renaissance

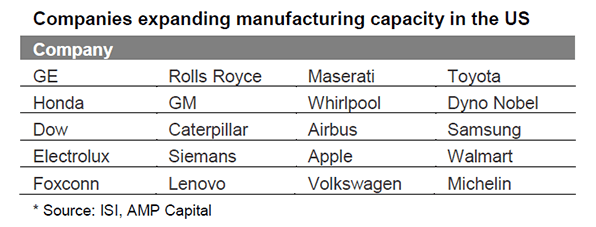

Numerous companies have announced that they plan to expand manufacturing production capacity in the US. This ranges from a plant to build a Honda super car to Apple bringing some component manufacturing home. The drivers have been a combination of:

- lower energy costs as cheap gas has seen electricity suppliers switch to gas, depressing the price of electricity;

- very low unit labour costs – as solid productivity growth and low wages growth have seen unit labour costs for manufacturers remain around 1980 levels; and

- the low $US after a decade long decline, which is still down 30% or so from 2001/2002 levels.

* Source: ISI, AMP Capital

As yet this has only resulted in a tentative rise in manufacturing production relative to overall GDP, but it is likely to improve further as the manufacturing base starts to expand again. Very different to Australia, but then again we have seen a doubling in the value of the $A over the last decade, somewhat higher wages growth and surging electricity prices…but that’s a different story!

Source: Bloomberg, AMP Capital

American ingenuity

Finally, underpinning all of this is American ingenuity and an economic system that encourages it and provides it with finance. The bulk of the new gadgets we get are developed in the US, it remains at the forefront of the IT revolution and its companies are world beaters. Since 1975, the Eurozone has given rise to just one of the firms to join the world’s top 500 companies, whereas 26 of them came from the US.

What does it mean for investors?

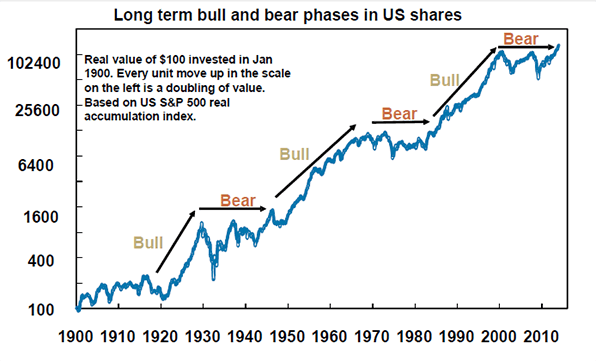

The key message is that the US is getting back in business (putting aside the winter freeze) with a potential to grow maybe as much as 0.5% pa more over the medium term compared to what otherwise would have been the case. There are several implications for investors. First, a stronger US economy is good for the global economy and supports the view that global share markets have entered a new secular (or longer term) bull market. Consistent with this, US shares have broken out to a new record high – both in terms of the S&P 500 price index and in terms of real returns after spinning their wheels since March 2000. See the next chart.

Source: Global Financial Data, AMP Capital

Second, the US looking stronger at a time when several emerging countries have hit a more difficult patch favours traditional global shares over emerging market shares. Finally, whilst US and hence global shares appear to have entered a new secular bull market, returns are likely to be more constrained than was the case during the last secular bull market that started in 1982. This is because starting point valuations for shares are not as attractive as in 1982 and the boost from falling inflation and interest rates won’t be repeated again in the years ahead as inflation is already low.