How to source income in a low interest rate environment

15th January 2013

In recent years, investors looking to source income have been attracted to the yields and perceived safety of term deposits. But, with term deposit rates expected to fall to less than 4% in 2013, investors should be considering other strategies that meet their needs. Alternative sources of income are available across the risk spectrum – through shares and listed property in the form of dividends, and through bonds in the form of coupon payments. We met with Jeff Brunton, Head of Credit Markets at AMP Capital, to discuss the opportunities available from corporate bonds.

Which factors are likely to determine the direction of cash and term deposit rates?

The rates on offer from term deposits are expected to fall to less than 4% in 2013. Factors determining the direction of term deposit rates in the future include the cash rate set by the Reserve Bank of Australia and banks’ funding requirements.

Although the Reserve Bank of Australia (RBA) has been reducing rates since October 2011, banks have only been passing on around four-fifths of cash rate cuts to lower mortgage rates. Given the headwinds coming in the form of the strong Australian dollar and government budget tightening, the RBA estimates the mortgage rate needs to fall to around 6% in order to stimulate growth in the economy. To achieve a mortgage rate of around 6%, we believe that cash rates will need to fall to 2% to 2.5% which is likely to lead to a further decline in term deposit rates. Indeed, Bank Bill Futures derivatives in the Australian market, which are the market’s best estimate of future cash rates, indicate that the cash rate will fall close to 2% in 2013.

There will also be important regulatory changes occurring in 2013 and beyond which will drive banks to design ‘new generation’ term deposits which have much reduced liquidity features relative to the term deposits investors are currently able to access.

What does this mean for investors looking to source income?

For investors who have an ongoing need for income and liquidity, they should be revisiting their investment strategy now. Alternative sources of income are available across the risk spectrum – through shares and listed property in the form of dividends, and through bonds in the form of coupon payments. At present, there are unusual dynamics playing out in the global credit cycle which present exciting opportunities in corporate bonds for investors looking to source income. For investors who have ongoing liquidity requirements, this can be provided through most actively managed bond funds which offer liquidity on a daily basis.

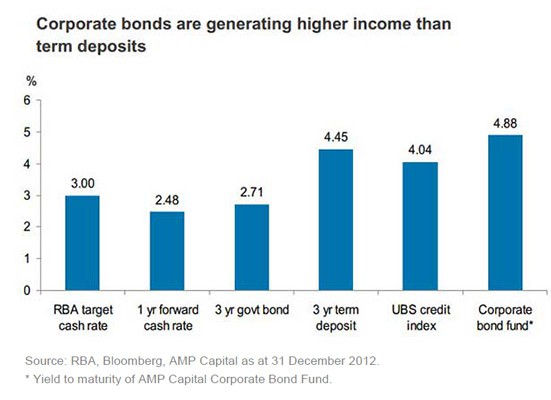

What opportunities are corporate bonds currently offering investors?

Corporate bonds are currently offering income in excess of government bonds and term deposits, as shown in the chart below. Although the yields on offer from corporate bonds may be volatile in the future, they are expected to remain high for the next few years, providing a good source of income for investors.

Corporate bonds are currently offering superior yield for risk, largely because of the dynamics playing out in the credit cycle. The credit cycle explains the growth and contraction of credit or debt in the economy that originates from consumers, corporates and governments. The direction and stage of the credit cycle is often touted as a subset of the business cycle, and is consequently a good indicator of what is happening in the overall economy. We are currently in a ‘de-synchronised’ credit cycle which is creating opportunities for investors in the corporate bond market. Governments and banks are displaying high debt levels. In contrast, corporates have much healthier balance sheets as they have reduced much of their debt.

However, corporate issuers are not being rewarded for their healthier balance sheets, and credit spreads (the excess yield offered by corporate bonds over government bonds) have subsequently remained high. Because a number of governments are yet to go into ‘repair’ mode, they are effectively contaminating the strong parts of the market (corporates), which means that these issuers are offering superior yield for risk. Why do we expect yields on corporate bonds to remain relatively high? The excess yield on corporate bonds over government debt is likely to remain high and volatile for the next three to four years, largely due to perceived risks generated by ongoing global government debt issues.

The European sovereign crisis is expected to take many years to resolve. In a number of European countries, such as Greece, Spain and Italy, debt to gross domestic product ratios remain high, signalling that these governments will continue to run up debt for at least the next two to three years. Despite the largest cuts to government spending in a generation, the US is still faced with a large debt that it needs to reduce. And in Australia, the Government recently abandoned plans to move their annual budget into surplus which will now see five years of rising debt, albeit from a very low level.

The excess yield on corporate bonds will provide an ongoing source of income for investors. And while we believe total returns from corporate bonds will be muted compared to previous years, they should still be higher than the return an investor can expect to achieve from government bonds and term deposits. What is the best way for an investor to access corporate bonds? To take advantage of a regular income stream from bonds, as well as reduce the risk of capital loss, investors should look towards an actively managed bond fund as opposed to investing directly in bonds.

For investors requiring a stable income stream, by investing in an actively managed fund, they are reaping the benefits of combining old and new bonds to result in stable income during different market cycles. By contrast, history has shown us that term deposit rates can fall quite drastically. As such, they are not a reliable investment for meeting medium to long term income requirements.

With rates set to fall on term deposits, the risk for an investor is that when they come to roll their investment in three months or one year, the rate will have fallen, and their ability to consume based on the income they are earning today will diminish. In determining whether a bond fund meets their income requirements, an investor should assess the duration of the fund. Duration is the length of time over which it is likely the investor will earn income from a security or a portfolio of securities.

For example, in a bond fund which holds bonds with maturities of three, five and seven plus years that are giving an overall yield to maturity of 5%, the return stream to the investor, if the bonds stay in the portfolio, will be 5% for the next three to seven years. Investors can now access corporate bond funds that have an annual income higher than term deposit rates. Of course, the income available from managed bond funds will differ from fund to fund, as it is subject to the yields and coupons of individual securities within the fund. How can an actively managed bond fund reduce the risk of capital loss? Investors should be mindful that, from a portfolio construction point of view, investing in bonds should not just be about generating income.

They should also offer a defensive component in an investor’s overall portfolio. Higher yields mean more credit and liquidity risks. Therefore, in order to lessen the risk of capital loss, it is essential that investors understand the securities they are buying. For those considering investing directly into listed bonds, they should be aware of subordinated instruments and hybrids. Although they may provide income, they generally also come with an increased risk of capital volatility. These are complex instruments, displaying equity and bond-like characteristics. In fact, many managed corporate bond funds don’t regard hybrids as ‘defensive’ securities, and hold them more for growth reasons than income.

Active bond managers will commonly adjust a bond portfolio’s duration (which is the weighted average duration of all the bonds in the portfolio) to protect the capital value of the fund. For example, a bond manager expecting interest rates to fall would normally ‘lengthen’ the portfolio’s duration by buying longer term bonds and selling shorter term bonds. This is because, in this circumstance, the price of a longer duration portfolio should rise more than that of a shorter duration portfolio. By investing in an actively managed, diversified fund, investors are able to spread portfolio risk. When investors have exposure to only a small number of securities, this exposes them to concentration risk in issuers, industries or geographies, and a systemic event can impact a large part of the portfolio. Source: AMP Capital