The Asean region has witnessed the rapid growth of fintech companies over the last decade. The trend of rapid fintech growth seems poised to continue into the future with robust investor interest in companies in the region. In 2017, fintech companies based in the Asean region received investments totalling $5.7 billion. A Deloitte report said that this was expected to be exceeded by 20 to 30 percent in 2018.

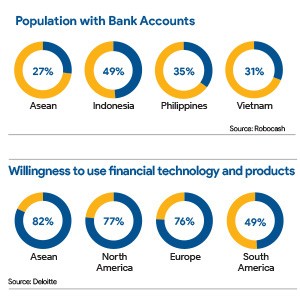

A 2019 report by Tech Collective further augments this view. It said “The Southeast Asia region is ripe for tremendous growth in the fintech industry in 2019.” The primary reason for the same, it said was the fact that only 27 percent of the adult population across the Asean had an actual bank account.

A report from international lender Robocash further clarifies the extent of the unbanked population and the fintech opportunity present therein. It says, in Indonesia, only 48.9 percent of the population had a bank account in 2017, but 54.8 percent borrowed money. In the Philippines, only 34.5 percent had a bank account while 58.6 percent of people had made borrowings. While in Indonesia, only 49 percent of the population had a bank account, in Vietnam, this figure is quite low at just 31 percent. This disparity between the banked population and population participating in financial activities present a huge opportunity for fintech companies in the region.

Ajit Raikar, co-founder and CEO at Validus Capital, a Singapore-based peer-to-peer lending fintech startup, further reinforced this view to International Finance. Citing consulting firm, KPMG, Raikar said, “There is an unmet need for access to basic banking services. Only 27 percent of the region’s 600 million inhabitants had a bank account in 2016.” This, he added, “is where fintech startups can come in to fill gaps and accelerate financial inclusion in the region.”

He further claimed that his company alone had facilitated over SGD230 million in financing for Singapore’s small and medium-sized enterprises (SMEs). This, he said had a positive impact on over 300,000 citizens of the island state-city, directly or indirectly.

He further claimed that his company alone had facilitated over SGD230 million in financing for Singapore’s small and medium-sized enterprises (SMEs). This, he said had a positive impact on over 300,000 citizens of the island state-city, directly or indirectly.

According to EY, there are more reasons than the one mentioned above as to why the region is witnessing a rapid adoption of fintech innovation. Its ASEAN FinTech Census 2018 report lists “rapidly expanding economies, young-urban-digitally-savvy population, increasing mobile and internet penetration apart from largely underserved, small and medium-sized enterprises (SME) and consumer markets by traditional financial institutions” as the other factors driving growth of fintech in Southeast Asia.

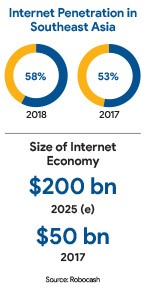

With regards to internet adoption, Southeast Asia is the fastest growing in the world. This was estimated at 58 percent in 2018, up from 53 percent in 2017. Citing Google and Temasek, a report by Robocash stated that the number of local Internet users was expected to reach 480 million people in a year in this region. The report further predicted that the internet economy in Southeast Asia would increase to $ 200 billon by 2025. This is a four-fold increase from the $ 50 billion in 2017.

So, while internet penetration is high, digitisation of financial services does not seem to have really picked up pace. According to a fourth quarter 2018 report by Cento, Southeast Asia is the fastest growing digital economy, although less than 2 percent of the economy is digitised. This huge digitisation gap further increases the growth potential for fintechs in Southeast Asia.

Justin Hall, partner at Golden Gate Ventures, an early-stage VC firm focusing exclusively on Southeast Asia, seems to concur with the earlier mentioned facts. When International Finance queried him about the unique promise he sees in Southeast Asia versus other regions, he said, “Southeast Asia is one of the fastest growing, dynamic markets in the world. It possesses some of the most populous markets. Its emerging middle class is a boon to local economies and technology adoption – from mobile phones to internet services, infrastructure to online payments – is rapid. In simplest terms, Southeast Asia is a new growth opportunity in the same way India and China were before it.”

Supportive governments

Apart from these, the Asean governments need to be credited for the growth of fintech in their respective regions. In an effort to make its population get used to a cashless or a digital payment system, these governments have launched various initiatives that help create a conducive environment for fintech.

Speaking on the same, Raikar said, “With many countries in Southeast Asia having a large unbanked population, governments today are embracing the ‘cashless society’ agenda more than ever before. Going cashless helps to create financial identities for these individuals and accelerate financial inclusion in the region.”

Speaking on the same, Raikar said, “With many countries in Southeast Asia having a large unbanked population, governments today are embracing the ‘cashless society’ agenda more than ever before. Going cashless helps to create financial identities for these individuals and accelerate financial inclusion in the region.”

Citing Singapore as an example, Raikar said, the government of this island city-state had launched initiatives such as the national QR code and NETS that further augur well for the future of fintech startups the region.

“In its push for a cashless society, the Singapore government has launched a national QR code standard to unify a fragmented e-payment landscape it has also deployed NETS, an electronic payment service provider, to centralise the e-payment systems, bringing cashless payment to hawker centres and coffeeshops nationwide. To incentivise more hawkers to use the e-payment system, NETS has also launched an initiative to ensure hawkers get faster access to their funds from NETS transactions,” he explained.

He further added that other countries in the Asean region such as Vietnam and Indonesia too were already working towards a cashless society. “Vietnam strives to become a cashless society by 2020 and reduce the number of cash transactions at large-scale retailers to less than 10 percent, while Indonesia has revamped its regulatory framework as it aims to become Southeast Asia’s digital hub by 2020,” Raikar said.

Meanwhile, in the Philippines, the country’s central bank has established a regulatory framework called The National Retail Payment System or NRPS to support digitisation of financial transactions. The objective of this is the establishment of a safe, efficient, and reliable retail payment system in the country. According to the central bank’s website, the key outcome of the NRPS is “to increase adoption of electronic retail payments from 1 percent electronic payments in 2013 to 20 percent electronic payments by 2020.”

In Malaysia, its central bank, the Bank Negara Malaysia had introduced a financial technology regulatory framework way back in 2016. Through this, the central bank sought to provide a regulatory environment that would be conducive for the deployment of fintech solutions. Its website states that this includes reviewing and adapting regulatory requirements or procedures that may unintentionally inhibit innovation or render them non-viable. As part of this process, the Financial Technology Regulatory Sandbox Framework (Framework) is introduced to enable innovation of fintech to be deployed and tested in a live environment, within specified parameters and timeframes.

Additionally, as recently as in September 2018, it launched the Digital Finance Innovation Hub in association with The United Nations Capital Development Fund and Malaysia Digital Economy Corporation. The objective of this was “to enable service providers, including financial institutions and fintech start-ups, to use technology in promoting inclusive finance, including through the introduction of products and services that meet the needs of the underserved in Malaysia.”

Such initiatives by the governments in the region further augment the growth of fintech in the region. Commenting on the same, Raikar said, “The friendly regulatory environment coupled with the desire to drive financial inclusion and become cashless societies, provide fintech startups ample room for growth and development. The future is promising for the industry.”

Commenting on the same, Joel Yarbrough, VP Asia Pacific at Rapyd, a global fintech-as-a-service startup with offices in London, Singapore, Silicon Valley, and Tel Aviv that enables any payment type for in-country or cross-border commerce, told International Finance, “I’m very positive on the role that government and regulators in the region have played in creating that emphasis, but at the same time there is no ‘one answer’, there is a mix of many different answers, and the market needs to be encouraged to find the right one for each segment or use case.

Things like interoperability, eKYC, strong authentication, and progressive regulation are all important, and the fintech industry overall benefits from governments innovating and competing with each other in these areas.”

Open to innovation and abuse

The interest of Asean governments in encouraging fintech is also because of the many technology and innovation advantages they bring to the table. Empowered by emerging technologies, such as artificial intelligence, blockchain, and machine learning, these companies could help offer basic financial services such as bank accounts, loans, credit cards, and insurance to the large population that currently do not have the same. Technologies like blockchain in particular could drive down operational costs of remittances that are currently expensively taxed. It would also help several SMEs that are currently not being served by the existing financial systems in the region.

Of course, as always, there are two sides to any coin and fintech too has some negatives. According to the Deloitte Singapore FinTech Festival 2018 report, the biggest risks related to fintech is its misuse for tax evasion, money laundering, or for making fraudulent transactions that bypass traditional financial systems.

The fourth and final reason that is boosting the growth of fintech in Southeast Asia is the openness to use fintech products. A November 2018 report from Deloitte conducted in partnership with Robocash Group stated that, of the respondents polled, 82 percent of Asean customers’ showed willingness to use new fintech technologies and products, compared with 76 percent in Europe, 77 percent in North America, and 49 percent in Latin America. The report further said that countries in the Asean region had the highest potential to grow their fintech markets up to 2020.

Yarbrough corroborated the Southeast Asian region’s fintech promise to International Finance. He explained, “Asean is a high growth, extremely digital, social, and mobile market. At the same time, there is a large population that is under-banked, under-supplied in credit, or that doesn’t have full access to international markets electronically. Given the openness to using the Internet for almost everything else, we see that same openness and education being a fertile ground for fintech adoption.”

Despite the obvious advantages of the region, accessing trained fintech talent is a challenge for startups in the region. Citing EY, Raikar said that “Three in five (60 percent) of Southeast Asia fintech companies surveyed found that they lack the tech talent required for their business.”

Recruitment firm Hays further emphasised the same with a focus on Malaysia. In a May 2019 article it was cited as saying that Malaysia was facing a shortage of talent to support the digitisation of its banking and financial services.

Natasha Ishak, senior manager for banking and financial services at Hays further explained that the previous few years had seen the introduction of various financial products and services, and this had affected talent shortage across various domains ranging from product development to contact centres and compliance departments.

That said, the governments in the region have already noticed this issue and are taking corrective measures. With regards to Singapore specifically, Raikar said, “Both the government and organisations in Singapore, have already taken steps to bridge this gap. These include initiatives such as The Adapt and Grow which aims to help Singaporean workforce transition into new job roles in growth sectors, and partnerships forged between corporations and educational institutions to create a vibrant entrepreneurial community such as NUS Enterprise setting up a cybersecurity startup hub with SingTel Innov8 as well as their collaborations with Singapore Airlines to promote the aviation industry.” This, Raikar said, will allow fintech companies to get the right talent needed and bridge the gap ensuring long-term sustainable growth.

Meanwhile, Yarbrough opined, “On the government side, I think smart university and workforce training are important, particularly in critical domains like machine learning.” He however also said that the region was ramping up quickly the development of talent required to operate in the fintech space. “We have people moving into the region, moving from traditional financial companies, but most excitingly an amazing base of young talent that is educating itself and scaling quickly,” he added.

Big companies also enter

So, whats interesting is it’s not just startups that are embracing fintech. Large established companies are also using their existing platforms to provide financial services by using technology. In Asean region, fintech pioneers include Grab, Lazada Group and Go-Jek. Grab which originally was in the transport business is now offering payments, rewards, and loyalty services apart from loans and insurance. On the other hand, retail company Lazada Group now also offers e-wallet payments and SME lending. Meanwhile, Go-Jek in 2018, spun off its e-wallet service Go-Pay as an independent app. By end of the year, this app had partnerships with almost 400,000 merchants helping transaction volumes to exceed $6 billion.

So while the Asean region definitely seems to be attractive for receiving new investments in fintech space, the question arises as to whether the fintech innovations in the region, especially in the payments space were reaching a saturation point. According to Justin Hall of Golden Gate, “We have barely scratched the surface of fintech. There is a still a huge amount of innovation and value-creation to be unlocked, and much of that is dependent on the new industries and verticals we will see emerging and evolving over the next few years.

The explosion of agent-led networks (‘social commerce’), gig economies, IoT-enabled products, and data collection means that financial services will need to scale and evolve in very interesting ways to keep up, and I think we’re going to see really intriguing use-cases here that we don’t see anywhere else.”

So to conclude, while large players are also diversifying into the fintech space, there seems to be scope for new innovative fintech startups to flourish as well in Southeast Asia. A perfect storm of supporting factors led has unleashed the fintech innovation spirit in Southeast Asia. Given the demographics, the openness to technology, the government support, and the quantity of investor funds flowing into the region, the pace of fintech innovation in Southeast Asia is set to accelerate in the future.