One source of uncertainty to the outlook for US monetary policy arises from the expiration of Janet Yellen’s term as Chair of the Federal Reserve (Fed) Board of Governors in February 2018, and whether President Trump will reappoint or replace her. Uncertainty arises also from the idea put forth by some members of Congress that the Fed should adopt a rules-based policy strategy, such as the eponymous rule designed by Professor John Taylor of Stanford University, who is also seen as a potential candidate to replace Chair Yellen.

The Board of Governors

The Board of Governors has seven members that are nominated by the President and confirmed by the Senate. Their term of office is 14 years, but most do not serve a full term. Together with the President of the New York Fed and four Presidents of the other 10 regional Federal Reserve Banks, they constitute the Federal Open Market Committee (FOMC), which sets US monetary policy.

The President also nominates the Fed’s Chair and Vice-Chair, who also must be confirmed by the Senate, for a four-year term of office. Chair Yellen’s term ends on February 3, 2018. Before her appointment as Chair, Yellen served as Vice-Chair, taking office in October 2010. Her term as a Board member will expire on January 31, 2024.

Chair Yellen has a long and successful record as a member of the FOMC. She served as a member of the Board of Governors from 1994-1997 and as President of the Federal Reserve Bank of San Francisco from 2004-2010. While Presidents often reappoint Fed Chairs that have been appointed by their predecessors, they are free to replace them. President Trump is currently in the process of determining whether to reappoint or replace Yellen. Many commentators believe he will nominate a new Chair.

Possible contenders

Speculation about a possible new appointment focuses on two names. The first is Jerome Powell, who has served as a Fed Governor since 2012, and who is seen as the favourite. Prior to that, he was Assistant Secretary and Under-Secretary of the Treasury under President George H W Bush. Before that, he was a lawyer and investment banker in New York.

The second candidate often mentioned is John Taylor, who was Treasury Under-Secretary for International Affairs, 2001- 2005, and who developed the Taylor Rule, discussed below, as a means of describing the way in which the Fed sets interest rates.

While these two candidates are the current favourites, it is of course possible that somebody else will be appointed, or that Chair Yellen will be reappointed.

Risk of rapid interest rate increases exaggerated

Since Powell and Taylor are viewed as more hawkish than Yellen, some market participants are concerned that the Fed will tighten monetary policy more quickly than previously expected. Another concern is that some members of Congress believe that in setting policy the Fed should behave in a more rule-like fashion, for instance by attaching greater weight to the Taylor Rule. A source of concern is that the Taylor Rule, in its original form, suggests that the Fed Funds rate should now be raised sharply.

But there are two reasons why markets may be overreacting.

First, the Fed Chairman does not set policy but merely chairs the meetings at which policy is set. The Chair’s influence on policy thus depends on his or her ability to persuade other FOMC members. Since they will not change, the Chair’s impact on policy will be limited.

Second, one component of the Taylor Rule, the assumption that the ‘neutral real interest rate’ is 2%, is now generally seen as far too high. To explore the consequences of this, it is useful to consider the Taylor Rule, which was first proposed by Professor Taylor in an article published in 1993 as a way to understand the interest rate setting behaviour of the FOMC from 1987-1992 in greater detail.

The Taylor Rule

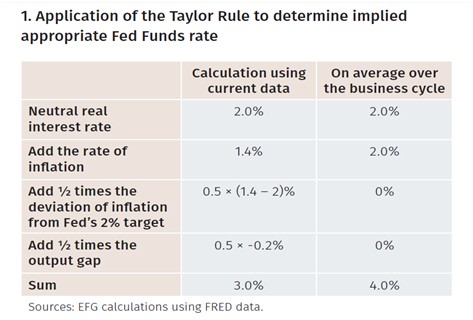

To compute the level of the Fed Funds rate suggested by the Taylor Rule (see Figure 1), one starts with the neutral real interest rate, which Taylor assumed to be 2%. To this, the current rate of inflation, 1.4%, is added together with half of the difference between the rate of inflation and the Fed’s inflation objective of 2%, that is, 0.5 × (1.4 – 2)% (Info Graph 1). Finally, half of the current output gap 0.5 × -0.2% is added for a total of 3%.2 With the target range for the Fed Funds rate currently at 1-1.25%, the Taylor Rule points to a need to raise it sharply.

Taylor’s analysis shows that the Fed’s interest rate changes can be captured surprisingly well by appealing solely to movements in inflation and in the output gap. This suggests that an interest rate computed using the Taylor Rule can serve as a useful reference point for the FOMC when setting monetary policy. Thus, when the actual Fed Funds rate deviates materially from that implied by the Taylor Rule, FOMC members should make sure that they understand why that is the case.

Info Graph 2 shows the actual Fed Funds rate and the rate implied by two versions of the Taylor Rule. In the first, inflation is measured by the GDP deflator, as proposed by Taylor, and in the second it is measured by the core PCE deflator, which is the FOMC’s preferred measure of inflationary pressures.

Interestingly, the Fed Funds rate was generally above the rate implied by the two Taylor Rules before 2003, and below it afterward. Moreover, there are large and persistent deviations between actual and implied interest rates. This suggests that policy makers also paid attention to other variables, and that policy judgement was important.

But while useful, it is easy to exaggerate the importance of the rule. In particular, there is no reason to believe that the rule is optimal – the rule was intended to capture the fed’s behaviour in a particular historical episode. Furthermore, there is no reason to assume that the neutral interest rate is fixed.

The neutral real interest rate

Indeed, many observers have argued that the neutral real interest rate has fallen over time. For instance, San Francisco Fed President John Williams has compared five estimates of the neutral real interest rate in the US and concluded that the average of these fell from 3% in 1986 to 2% in 2007. Following the onset of the financial crisis in 2008, it fell further to 1% in 2009 and to about 0.5% in 2016. Of course, forecasts differ; the five estimates that President Williams investigated ranged from 0% to 1% in 2016.

Another way to get a handle on the neutral real interest rate is to look at FOMC members’ predictions of inflation and the Fed Funds rate in the ‘long run’, which the Fed releases on a quarterly basis. These forecasts can be interpreted as FOMC members’ beliefs about the average inflation rate and Fed Funds rate in the future, once any temporary disturbances have dissipated.

In September 2017, the average long-run inflation rate was 2% and the average Fed Funds rate was about 2.8% (in contrast to the Taylor Rule which implies that the Fed Funds rate should average 4% over the business cycle, as shown in the table above). This implies that FOMC members believe that the neutral real interest rate has fallen to 0.8%.

Overall, the interest rate indicated by the original Taylor Rule is unlikely to be appropriate now because the neutral real interest rate has fallen sharply since the financial crisis. Rather than being 2% as assumed by Taylor 25 years ago, it may be 1% or perhaps even as low as 0%. Adjusting the Taylor Rule for this decline leads it to suggest that an appropriate level of the Fed Funds rate is currently in the range of 1-2%. The idea that attaching weight to the Taylor Rule would lead the Fed to raise interest rates sharply thus seems misguided.

Stefan Gerlach is Chief Economist at EFG Bank