Today, with the acceleration of climate change and global climate activism reaching a fever pitch, there are virtually no corporate organisations or governments in the world that are environmentally conscious. What if you could invest in financial instruments with predictable returns that finance projects related to energy efficiency, pollution control, clean transportation, sustainable water management, and development of environment-friendly technologies? Enter Green Bonds or Climate Bonds that are asset linked securities backed by the issuers balance sheet to finance solutions to the earlier mentioned kinds of environmental challenges.

In 2012, global Green Bond issuances amounted to only $2.6 billion. That situation has changed dramatically since then. According to a report by Climate Bonds Initiative and others, the labelled bond market size for Green Bonds in 2018 was $167.6 billion and cumulative issuances since 2007 have now hit $521 billion.

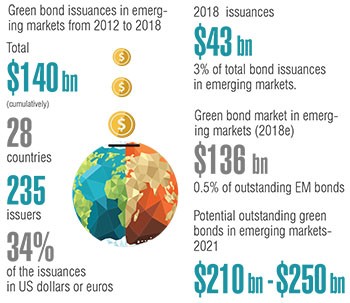

In 2018, Green Bond issuances by emerging markets institutions and governments amounted $43 billion or just 3 percent of all regional bond issuances, according to the World Bank’s International Finance Corporation (IFC). Emerging markets should be the centre of global Green Bond issuances considering that the emerging market nations that are facing the worst effects of climate change, compared to the developed world. So what can be done to raise the share and profile of emerging market Green Bonds? And how do you convince emerging market issuers and investors about the value proposition of Green Bonds?

According to the IFC, emerging markets are not only the most exposed to climate change risks, but also face an unprecedented challenge to de-carbonise their economies, while maintaining a sustainable economic development trajectory. IFC says that one of the biggest challenges faced by emerging markets is balancing increased infrastructure financing with environmental and social safeguards to ensure that new infrastructure needs meet climate-smart requirements in the quest to build sustainable infrastructure. But, where will the capital come from?

$147 trillion of institutional capital in the world

There is $147 trillion of private institutional investor capital in the world, according to IFC. Much of this amount is located in developed markets and Organisation for Economic Cooperation and Development (OECD) countries alone account for $84 trillion.

Developed countries mainstream institutional investors commonly have little exposure to emerging markets bonds and long-term infrastructure financing projects, possibly due to the scarcity of appropriate investment opportunities. Jean Marie Masse, chief investment officer, Financial Institutions Group, at IFC told International Finance that leveraging this capital remains a challenge. In the developed world policy makers, issuers, and investors have mobilized green bond issuances. The European Union (EU) took significant steps through a proposal for an EU Green Bond Standard. However, a similar mobilisation is missing in the emerging markets and investors are not aware of such investment opportunities, says Masse.

The World Bank’s IFC is a pioneer in the Green Bond market. Since launching the Green Bond Program in 2010, IFC remains one of the world’s most prolific issuers of green bonds. In 2013, IFC was the first issuer to list a billion-dollar green bond in the global market. This was heralded as a landmark transaction which proved green bonds as a mainstream product. To date, IFC has issued around 150 green bonds in 16 currencies worth almost $10 billion.

With regard to why the emerging markets lag in Green Bond issuances and investment, Jean Marie Masse of IFC points to the lack of clear environmental, social, and governance (ESG) management practices in emerging markets. “IFC has identified a gap in the market: the absence of a global standard on green bond external reviews. As a result, green bond investors often receive incomplete or incomparable information across their green bond investments.

The harmonisation of external reviews, including second opinions and other related services, will contribute to the development of accountability and quality standards for the emerging markets green bond market,” Masse told International Finance. What is the reason for the gaps in the data quality in the emerging markets? According to Masse, the gaps in in emerging markets is due to the fact that historically issuers have not been formally required to report their internal initiatives on ESG factors. This variations in data quality makes it difficult for investors to determine the quality of ESG analysis, as well as the relevance of this analysis to long-term financial results.

Most developed segment of thematic impact bonds

As of now, the Green Bond market is today the most developed segment of thematic impact-oriented bonds. Green bonds deliver several benefits to issuers and investors. The main benefit for issuers is that they can target a larger investor base by attracting a dedicated pool of green and socially responsible investors. Positive publicity and media coverage are the other softer benefits of issuing a Green Bond. According to data from Bloomberg Barclays Indexes, in the euro market, green bonds returned 0.34 percent in 2018, while the overall investment-grade market returned 0.41 percent. In addition to comparable returns, Green Bonds provide an additional element of transparency to ensure that the funds are used to invest in environment friendly assets.

Nuru Mugambi, the curator of the Kenya Green Bonds Program, and a director of Kenya Bankers Association, explains that the Green Bond market is skewed in favour of developed nations because the development finance institutions first pioneered Green Bonds. “However, we have seen more activity in the past two years in the emerging markets and I think such activity should be supported and amplified,” she told International Finance.

According to Mugambi, in developing countries, the limitations to expanding the market for Green Bonds include the need for market awareness and understanding, as well as, policy bottlenecks and capacity for the issuance of green bonds, including pipeline identification.

Climate Bonds Initiative Head of Latin America, Thatyanne Gasparotto told International Finance that key aspect here is enhancing market participants’ understanding of green bonds, its processes and opportunities. “By building local capabilities across issuers, governments and investors, we can develop a green investment pipeline,” she adds.

Sovereign green bonds as inspiration

With regard to developing a solid pipeline of green bonds in emerging markets, Thatyanne Gasparotto is of the opinion that sovereign bonds from national governments provide a powerful signal to local stakeholders, both potential issuers and investors, about the value proposition of green bonds. “In Latin America, we are already seeing the impact of the Chilean bond in stimulating debate. We saw a similar effect following the Nigerian and Fijian sovereign Green bond issuances in emerging markets, and in Europe from the initial Polish and French issuances,” Gasparotto told International Finance.

The second action point she suggests is building a green bond market from the ground up. She calls for active market development programmes at the local level involving all the key finance stakeholders, including regulators, issuers, major banks and insurers, verifiers, pension funds, and other potential investors. It is key to identify sectors, opportunities, investment pipelines all with the aim of getting the first round of bonds into the market, according to her. She also calls for active involvement and support from the relevant multilateral development banks and development financial institutions in issuing Green Bonds.

In March 2018 Indonesia issued the very first sovereign green sukuk in US dollars. The five-year issuance raised $1.25 billion and, as expected, it reached a broad range of investors including Islamic, conventional, and green investors. In fact, the Indonesian green sukuk was oversubscribed, signaling the growing market demand for sustainable and responsible investments or green bonds. In February this year Indonesia again issued another green sukuk worth US$ 750 million with a five-and-a-half-year maturity period.

With regard to the Indonesian green sukuk issuance, James Kallman, the Chief Executive Officer of Praxity network member firm, Moores Rowland Indonesia (MRI), told International Finance, “It’s good news anytime a bond’s oversubscribed and this is pretty impressive, particularly for a country that historically has a low Islamic finance penetration.”

Another emerging markets sovereign green bond pioneer is Nigeria, which issued the first Climate Bonds certified sovereign green bond by an African nation in 2017. The five-year debt issuance of N10.69 billion due 2022 will see proceeds used to invest in projects that would reduce Nigeria’s carbon emissions by 40 percent by 2030. In June this year, Nigeria’s Debt Management Office announced that the country’s second sovereign green bond offer has been oversubscribed by 220 percent. The offer for N15 billion yielded a total subscription value of N32.93 billion. Confirming the success of the African nation’s green bond programme, the DMO said that the number of subscribers for the second issue had doubled when compared to the first issue in December 2017.

In Africa, the Kenyan government has been very progressive in developing environment-friendly policies and signalling the market towards promoting a green and circular economy. “Together with the Green Bonds Program Kenya partners we also are engaging the National Treasury to see how to incentivise innovations, such as green bonds, through fiscal policy that attracts both issuers and investors,” says Mugambi about the prospects of green bond issuances in Kenya.

China, the undisputed green bonds leader in Asia

In Asia, no discussions about green bonds can be completed without mentioning the giant strides that China has made. China’s official China Daily newspaper said that the country’s green bonds revolution is part of a project to turn the country from the biggest global source of environmental pollution to the global leader of climate change mitigation. In 2018, Chinese institutions issued $30 billion worth of green bonds that met international green bond classification norms.

James Kallman of Moores Rowland Indonesia says that, with three of the world’s four most populous countries and two of the largest democracies in Asia, including Indonesia, Asia Pacific is the region where we can expect greater attention and growth in green bond issuance, particularly given the multi trillion-dollar infrastructure needs. “As with most products and services, no company can ignore the China market and China is embracing green finance in full throttle. They have announced huge green bond issuance plans for the Belt and Road Initiative, plus domestically there may be no bigger threat to the leadership than the environmental concerns of the population,” adds Kallman.

But in the emerging markets, were the thinking of investors in driven by value, how do you convince investors that Green Bonds have a value proposition beyond ethical investing and safeguarding the environment? James Kallman tells International Finance, “Ethically managed companies not only make society better, they also have strong brand identification and consistently produce better returns over time. There is simply no bigger ethical issue today than climate change and in a highly corporatised, globalised world, corporations have a higher recognised responsibility not only not to do bad, but to do good.”

Development financial institution IFC says that to develop the Green Bond market in emerging markets, the institution will work on model green bond transactions issued by emerging markets issuers, release market research reports to disseminate information about the opportunities in green finance in emerging markets and develop tools to communicate about it. “Mobilising public and private institutional investors to deploy billions of dollars in capital for climate investments is essential to alleviate the impact of climate change.

The award winning Amundi Planet Emerging Green One (EGO) Fund does just that: as the largest green bond fund in the word, the fund is helping to scale climate finance in emerging markets,” says IFC’s Jean Marie Masse.

How do you ensure that green bonds are actually green?

Green bond investors need to be wary of ‘greenwashing’ of projects that are not environmentally friendly. A power producer in China, for example, once issued green bonds worth $150 million for a 2000MW coal fired power project. How do investors ensure that Green Bonds are actually green? Climate Bonds Initiatives Gasparotto says that the emerging markets have several guidelines – the Green Bond Principles and Climate Bonds Standard, for example. “There are several stock exchanges in Latin America that already have green bond listing guidelines with others under consideration. So there are developments at market level happening now,” she says.

A consortium of the world’s leading investment banks established best practice guidelines called the “Green Bond Principles” (GBP) in 2014. Ongoing monitoring and development of guidelines is now conducted by an independent secretariat hosted by the International Capital Market Association (ICMA). The GBP outlines the required transparency, accuracy, and integrity of information to be disclosed and reported by issuers to stakeholders. However, the Green Bond Principles do not provide details on what constitutes ‘green’.

Moores Rowlands’ Kallman says that while there are several similar standards, over a period of time it is inevitable that the most vigorous, most consistent, and most trusted one will become the accepted as the golden standard. Kenya, for example, has established a Green Bonds Program which has taken a comprehensive approach that incorporates international best practice into the local context.

The programme partners include Kenya Bankers Association (KBA), Nairobi Securities Exchange (NSE), Climate Bonds Initiative, FSD Africa, and FMO. “The programme has adopted the International Capital Market Association (ICMA) Principles and Climate Bonds Standards for green bonds. Moreover, the Kenya Capital Markets Authority has released issuer guidelines that recognise these two global standards as acceptable standards for green bond certification, says KBA’s Nuru Mugambi.

The GBP recommends that the use of proceeds to be disclosed in the form external reviews at the time of green bond issuances, and then through annual impact reports released by green bonds issuers. IFC conducted a study to analyse the scope and quality of ESG data collected by leading ESG data providers and identified market constraints. First, there are gaps in data reported by companies in the emerging markets. Second, ESG data providers use proprietary ESG scoring frameworks, which differ with respect to material relevance, indicator selection, and weightage. These differences result in conflicting ESG analysis and scores. Third, ESG reporting standards and guidelines differ across and within emerging markets. Even when companies report on the same topics, the data they report may not be comparable.

IFC for the use of AI and ML in ESG management

To solve these challenges, in the first half of 2019, IFC has explored ways to improve material ESG reporting, including working with an ESG data provider to increase the scope of coverage of emerging market issuers as well as broadening the coverage of collected ESG indicators. Jean Marie Masse of IFC told International Finance that IFC is also exploring ways to use of artificial intelligence and machine learning to support ESG data collection and analysis. He observes that opportunities exist to complement IFC’s work with ESG data providers to expand coverage of emerging market issuers and widen real-time information collection consistent with the IFC ESG Performance Indicators using AI and ML.

“Overall these efforts will play a key role in increasing market transparency and catalyse additional opportunities and investments in quality emerging markets green bonds. This is fully in line with IFC’s developmental mission and the green bonds in emerging markets are at the beginning of what we expect will be a fast-growing pace of new issuances meeting mainstream investors investment criteria, mobilising critical funding to help emerging markets cope with the consequences of climate change,” says Jean Marie Masse.

James Kallman of Moores Rowland Indonesia tells International Finance that mass adoption and mainstreaming of green bonds is inevitable, including in emerging markets. “Corporations are for profit animals and thus will follow consumer preferences, and relatively quickly so, in this age of information and disruption. Take the case of electric vehicles. Previously a niche space for a few brand lines and, of course Tesla, today there will be no automobile companies without an EV strategy. And this industry is a case in point for the entire green economy. There have perhaps been few companies in history with a lower cost of funding than Tesla. No capitalist company wants to ignore those funding benefits, the unique branding, or the consumer and institutional loyalty,” says Kallman.