Human trafficking is a global issue and cannot be ignored. It has emanated from former Eastern Bloc Europe, since the fall of the Berlin Wall, and the U.S. State Department annual report on human trafficking has ranked 23 countries in tier 3, the lowest possible mark when it comes to abating this crime. Drug lords and other bad actors target women, who are disproportionately trafficked as a cash source through forced labor or prostitution. The issue of human trafficking has worsened over the past four or five years because of porous European Union borders coupled with people desperate to flee war-torn areas, oppressive regimes and conflict zones. For example, the International Organization for Migration estimates a 600% spike in the number of potential humans being trafficked (mainly from parts of Africa) and entering Italy. These confluent dynamics make stopping human trafficking extremely difficult.

Human trafficking is a predicate offence to money laundering and terrorist financing. It is considered a financial crime, because it is a source for bad actors to gain funds and as such, companies in all industries, and especially financial institutions, have a mandate to disclose to regulators their efforts to wipe out human trafficking.

Their efforts are part of a robust financial crime compliance regime that all banks must have in place, as designated by global regulators. Central to regulatory compliance is automated screening using highly specialized software, name matching and other forms of patterned data that are then used in company communications to regulators. In other words, technology, data and analytics plays an extremely important role in identifying human traffickers while ensuring banks comply with regulations and operate efficiently.

Each year we issue the True Cost of AML (anti-money laundering) Compliance study. The goal is to understand the challenges financial institutions face when it comes to fighting financial crimes, like human trafficking, money laundering and terrorist financing. Through awareness, these issues can be resolved and the compliance function can focus more energy on stopping more financial crimes, which ultimately benefits society.

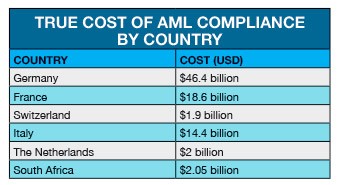

We recently conducted the EMEA edition of the True Cost of AML Compliance study where we researched Germany, France, Switzerland, Italy and The Netherlands in 2017 and South Africa in 2018. The true annual cost for these countries totaled USD85.4 billion. Table 1 outlines the annual cost per country.

Consistently the research showed across each country that AML compliance costs have risen in the past two years by about 20%, and an overwhelming majority (90%) of the respondents think the costs will continue to rise by double digits for the next two years, especially in the areas of compliance and sanctions screening. What variable is causing this cost upsurge? Labour.

Much of the AML Compliance function continues to be manual. In fact, the manual nature of this function attributes nearly 75% of costs to compliance. A True Cost of AML Compliance survey respondent from a Swiss financial institution said, “Complex procedures and approval by various authorities is not only a time-consuming task, but it also costs our firm a fortune to comply with the AML process.” Labour resources represent a significant component of compliance spend and activities, and this expense burdens firms, which causes a decrease in employee productivity and loss of prospective customers.

A truth stands: if labour continues to be a significant component of AML compliance, then overall costs will continue to increase. Why in the most technologically advanced era is compliance still so manual? The answer lies in the due diligence process.

Not surprisingly, the time required to perform customer due diligence has a significant impact on overall AML compliance costs, and firms in Europe reported long processing times across customer types. Even for domestic retail customers, who should face the simplest requirements, no respondents reported being able to complete due diligence in less than one hour. A majority of the respondents indicated they spend three to eight hours on domestic retail customers, with an average time of about seven hours.

Of interest is that financial firms spend more due diligence time on those entities that represent a smaller portion of new monthly accounts – namely, corporate customers. This resembles the “80 / 20” rule whereby most cost is consumed for a minority of customers. A “catch-22” exists. Corporate accounts are profitable but more complex than retail customers. With more complicated ownership structures, subsidiaries and overseas relationships, manual efforts can take substantially longer, increase labour costs, heighten customer friction and actually erode profitability.

A survey respondent from an Italian financial institution said, “The lack of a unique view of the customer forces our office to import data from different sources and channels and store them in multiple systems, so the process is frantic, tedious, and costly. This hampers our productivity.”

Alert processing times are significant and expected to get worse, contributing to increased costs and customer friction.

Most participating firms reported that alerts of any type take three or more hours to clear, with average times ranging from eight hours for KYC/due diligence alerts to 21 hours (nearly three business days) for AML transaction monitoring alerts.

KYC/customer due diligence alerts represented the greatest variation across countries. Firms in Italy were more likely to clear these alerts quickly (with an average time of 5 hours), whilst firms in the Netherlands were more likely to take a longer time (average of almost 10 hours). The challenge of clearing alerts is likely to get worse. More than half of firms who participated in the study (58%) expected alert volumes to increase by an average of 12 per cent. Significantly more Swiss financial institutions (78%) were likely to indicate expected increases.

The combination of increasing customer due diligence requirements, lower productivity and continued reliance on manual resources means that AML compliance has a meaningful negative impact on customer acquisition. There is a strong correlation between respondents’ ratings of AML compliance impact on customer acquisition and on overall productivity. This impact was cited as moderately negative by 72 % of firms. Similar to LoB productivity, firms in France and Germany are slightly more pessimistic about the impact on customer acquisition than firms in other countries (76 % and 78 % respectively); banks are more pessimistic than investment firms, likely due to the faster pace and volume of transactions on the banking side.

Customer friction during the on-boarding process costs European financial institutions prospective customers (73 per cent of respondents reported losing up to 4 per cent of prospective customers). For those prospective customers who do not leave during on-boarding, delays cause more than just frustration from waiting. They actually can cost customers money based on not being able to move forward with transactions. This is not a good way to start a new customer relationship; in fact, it likely leads to loyalty erosion faster compared to those who start out on a positive note. Expressed as a percentage of new account applications, almost half (42 per cent) of firms indicated between 6 per cent and 10 per cent of new accounts are delayed – similarly across countries and different types and sizes of firms. That reality can translate to a sizeable number of angry new customers who very quickly become high risk of churn at some point.

Something has to give.

Bank compliance functions are operating in an era of heavy operational workload. No doubt. Within this framework, most survey respondents indicated that streamlining or improving the efficiency of the KYC/customer due diligence processes is a priority for their organization. Overall, this aligns with concerns across countries regarding lost productivity and customer friction that is costing financial firms in terms of actual expenses and lost customers. Even more important, rising costs and new / ever-increasing regulatory requirements will necessitate more AML compliance process efficiencies; the role of technology and data are playing a role to relieve much of the burden financial institutions face with AML compliance.

Many survey respondents have already adopted shared interbank compliance databases and unstructured text data analysis, in-memory processing [what does this mean?, and cloud-based KYC utilities. Fewer firms use machine learning and artificial intelligence but adoption is expected to be widespread within five years. Unstructured audio and video data analysis are seen as relevant but less mature and further out for many. Not surprisingly, large firms (more than USD50 billion in assets) with their large compliance budgets are more likely than small firms to have implemented or be planning to implement these technologies.

Use of technology reduces the manual intensity of AML compliance, which enables compliance analysts to do their jobs more efficiently. This streamlining, especially of the due diligence and KYC processes, helps banks in their efforts to stop human trafficking.

For example, when a bank screens its customer list against a worldwide dataset using technology and linking, they can make sure they are not doing business with human traffickers, associates of human traffickers, money launderers or any other type of bad actor, thus curtailing human trafficking. Advanced linking technology is important because it enables the return of only relevant intelligence so that a financial institution can more accurately pinpoint if someone it is doing business with is a bad company or bad actor.

Human trafficking works in the dark shadows of the world. Technology, data and analytics are the tools financial institutions are using to put pieces of intelligence together to see where they might fit unwittingly in this crime. Additionally, technology, data and analytics gives companies intelligence to understand the scope of the problem and arms them with knowledge. As a result, companies can ask better questions, notice odd patterns and then reach out to their law enforcement agencies to shine a light into the dark shadows and stop human trafficking by stopping the flow of money associated with human trafficking.

Thomas C. Brown is the senior vice president of LexisNexis Risk Solutions in charge of U.S. commercial markets and global market development.